As costs continue to rise and buyers are priced out of their local market, Redfin has found that the length of time a home is on the market for is rising as a result.

In the four weeks preceding July 17, a new report from Redfin authored by Tim Ellis revealed that the average single-family home remained on the market for 19 days, one day longer than the same period last year, but well under the 60 days recorded from before the pandemic.

This marks the first time since the pandemic started over two years ago that the median time on market has posted a year-over-year gain.

The report also found that pending home sales took a 15% hit, decreasing more than they have since May 2020, while inventory posted its largest gain since August 2019, despite the fact that fewer homes are hitting the market than this time last year.

“Buyers, who earlier this year had to race to beat the competition, can now take their time touring homes and perhaps even wait to see if sellers drop the price,” said Daryl Fairweather, Redfin’s Chief Economist. “Still, few homes are being listed, so if your dream house hits the market, you should negotiate hard, now that you have the power to. The value may fall in the near term, but if you plan to live there for five or 10 years you will almost certainly gain home equity over that horizon. Sellers, on the other hand, may want to list sooner rather than later, before prices fall more.”

Other key facts found by Redfin include:

- For the week ending July 21, 30-year mortgage rates rose to 5.54%. This was down from a 2022 high of 5.81% but up from 3.11% at the start of the year.

- Fewer people searched for “homes for sale” on Google—searches during the week ending July 16 were down 23% from a year earlier.

- Touring activity as of July 10 was down 2% from the start of the year, compared to a 22% increase at the same time last year, according to home tour technology company ShowingTime.

- Mortgage purchase applications were down 19% from a year earlier during the week ending July 15 to the lowest level since April of 2020, while the seasonally-adjusted index was down 7% week over week.

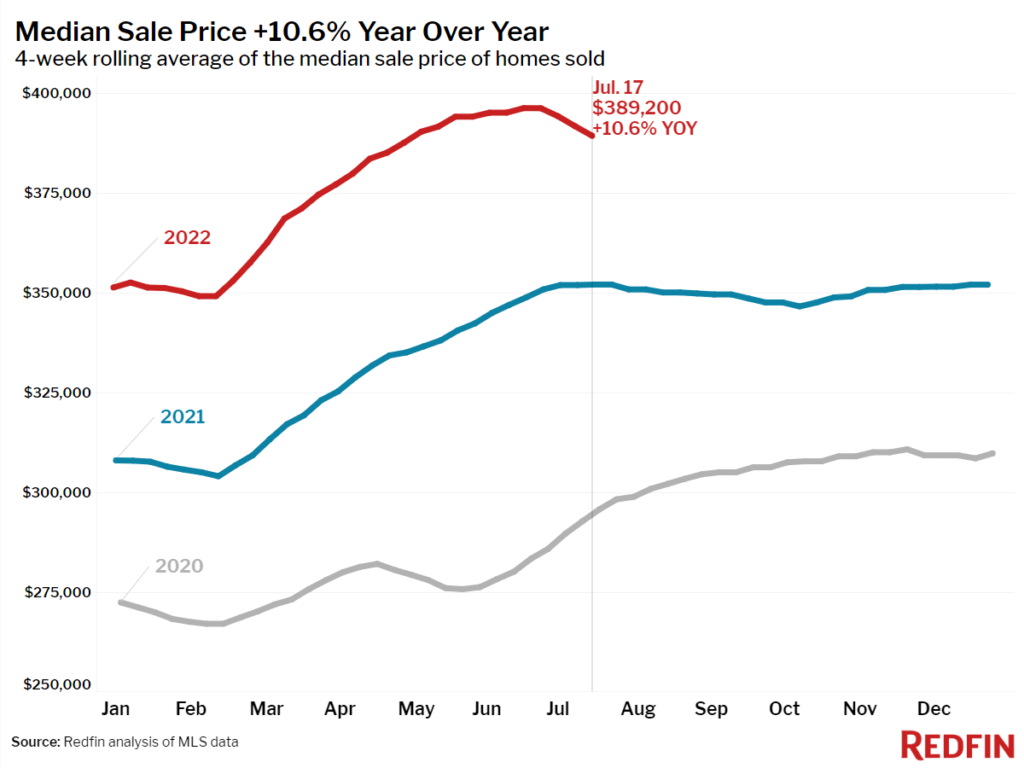

- The median home sale price was up 11% year over year to $389,200. This was down 1.7% from the peak during the four-week period ending June 19. A year ago the median price rose 0.9% during the same period. The year-over-year growth rate was down from the March peak of 16%.

- The median asking price of newly listed homes increased 14% year over year to $396,448, but was down 2.8% from the all-time high set during the four-week period ending May 22. Last year during the same period median prices were down just 0.8%.

- The monthly mortgage payment on the median asking price home hit $2,389 at the current 5.54% mortgage rate, up 45% from $1,650 a year earlier, when mortgage rates were 2.78%. That’s down slightly from the peak of $2,486 reached during the four weeks ending June 12.

- Pending home sales were down 15% year over year, the largest decline since May 2020.

- New listings of homes for sale were down 3% from a year earlier.

- Active listings (the number of homes listed for sale at any point during the period) rose 3% year over year—the largest increase since August 2019.

- 41% of homes that went under contract had an accepted offer within the first two weeks on the market, down from 46% a year earlier.

- 28% of homes that went under contract had an accepted offer within one week of hitting the market, down from 33% a year earlier.

- 49% of homes sold above list price, down from 54% a year earlier.

- On average, 7.3% of homes for sale each week had a price drop, a record high as far back as the data goes, through the beginning of 2015.

- The average sale-to-list price ratio, which measures how close homes are selling to their asking prices, declined to 101.4%. In other words, the average home sold for 1.4% above its asking price. This was down from 102.1% a year earlier.